PRSA’s for Employees

Free-Photos / Pixabay

Why should I plan for my retirement?

When you retire, you’ll expect to maintain the

same standard of living, yet have more time to

spend with your family, pursue leisure activities

and so on. Research shows that we are now

living much longer. This means we will need more

income for a longer retirement.

Would the State Pension (Contributory) for a

single person, of currently €233.30 per week

(increasing to €238.30 on 1st March 2017), be

enough for you to maintain your existing standard

of living? If that’s the only income you have when

you retire, it will certainly mean a big fall in your

standard of living. Not a nice thought, but one we

all need to consider. Added to this is the concern

that the State Pension will not be paid until age 68

for people born on or after 1st January 1961.

A PRSA (Personal Retirement Savings Account)

provides you with the opportunity to plan wisely

for your retirement.

Am I eligible to take out a PRSA?

If you are employed full-time, part-time, or even

participating in a job share, you may take advantage

of your employer’s Group PRSA arrangement

provided you are not already in a company

pension scheme. If you are already included in your

employer’s occupational pension scheme you may

only take out an Additional Voluntary Contribution

PRSA, subject to your scheme rules.

How flexible is a PRSA?

A PRSA is very flexible – you can start off by putting

a little aside and then as your income grows so too

can the amount you save. As well as increasing your

contributions, you can also decrease them at times

when you aren’t as financially well off. You can even

stop your payments and then restart them at a more

convenient time.

In addition, you can also make lump sum payments if

you wish to boost your PRSA.

What are the benefits of joining

my employer’s Group PRSA

arrangement?

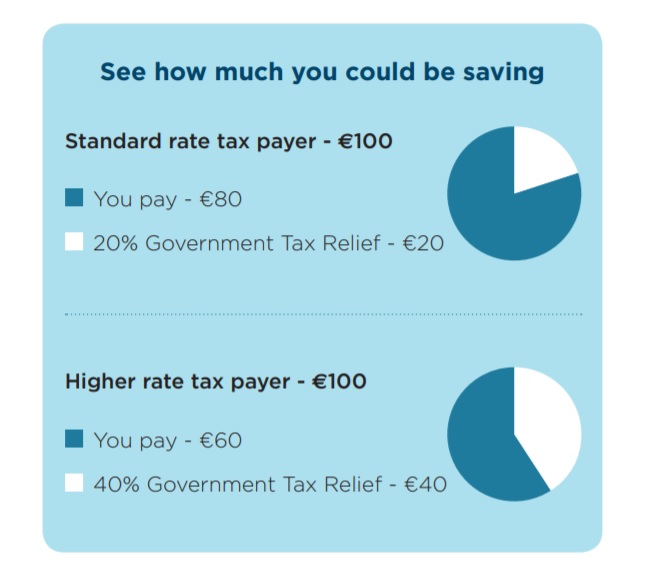

- Pay less tax – you can avail of generous tax

relief on your contributions, tax free growth on

your investment and a retirement lump sum of

which some or all may be taken tax free. - A wide range of investment options – You can

choose the fund or combination of funds which

best suit your needs. - Convenience – Your employer will make the

deductions from your salary/wages and forward

them to your PRSA provider for investment. The

amount deducted from your salary for your PRSA

contribution will appear on your payslip. - Employer contributions – If your employer has

committed to making contributions to your Group

PRSA account, this will help boost your retirement

income prospects. - Ownership – Your PRSA is personal to you and will

remain your asset even if you change employment.

Comments are closed.